Every intangible asset valuation eventually runs into the same bottleneck: the numbers. Revenue attributable to the brand. Operating margin on the customer book. Headcount and salary detail for the assembled workforce. R&D spend over the last five years. Tax rate. Discount rate inputs. None of that comes out of thin air — it comes out of the ledger. And until the ledger and the valuation workflow are connected, every engagement starts with a week of spreadsheet wrangling that nobody enjoys and almost no one audits.

Data import inside Opagio Intangibles was built to remove that bottleneck. The Valuator connects directly to Xero and QuickBooks for cloud-accounting customers, accepts structured CSV uploads from any other system (Sage, NetSuite, FreeAgent, Excel exports), and runs every imported figure through a chart-of-accounts mapping layer that ties ledger lines to the inputs each valuation method actually needs. The result is a single, audited source of truth that feeds Relief from Royalty, MPEEM, Replacement Cost, With-and-Without, Greenfield, and Market — without retyping a number.

This guide walks through how data import works, what the mapping layer does, and why a clean accounting integration is the difference between a valuation that takes a week and a valuation that takes a morning.

3

Supported import paths

6

Valuation methods fed by one dataset

5+

Years of P&L history typically pulled

1

Mapped chart of accounts

Why Data Import Is the Real Bottleneck

Every intangible asset valuation methodology — whether it sits in a Big Four PPA report, a fund's portfolio review, or Opagio Intangibles — needs the same handful of financial inputs. The methods differ in how they combine those inputs, but the underlying ledger lines are largely shared.

A complete valuation typically draws on:

| Input |

Where It Lives |

Used By |

| Revenue, by segment or product |

Sales ledger, accounting platform |

RFR, MPEEM, Greenfield, Market |

| Operating margin and contribution margin |

P&L, allocated cost data |

MPEEM, With-and-Without, Greenfield |

| Operating expenses by line |

P&L |

Replacement Cost, Greenfield |

| Headcount, salary, on-costs |

Payroll, HR system |

Replacement Cost (workforce), Greenfield |

| R&D and development spend |

P&L, capitalised intangibles |

Replacement Cost (technology), Capitalisation |

| Marketing and brand investment |

P&L |

Replacement Cost (brand), RFR cross-check |

| Tax rate and effective tax |

Statutory accounts, tax return |

All DCF-based methods |

| Five-year trend on each of the above |

Historical accounts |

Growth assumptions across all methods |

Pulling those inputs by hand is the part of every valuation engagement that consumes the most time and introduces the most error. Numbers get transposed. Categories get re-cut between management accounts and statutory accounts. The "marketing" line one valuer used is different from the "brand investment" line the next valuer used. By the time the valuation actually gets done, half the assumptions have been shaped by what was easy to extract rather than what was right.

★ Key Takeaway

The biggest threat to a defensible valuation is not the methodology — it is the data pipeline behind it. If the underlying numbers cannot be traced back to a single, audited source, every assumption in the workflow is suspect.

The Valuator's data import layer exists to remove that threat. It pulls the ledger lines once, maps them once, and reuses them across every valuation method. The audit trail is the chart of accounts itself.

Three Ways to Get Your Data In

The Valuator supports three import paths. Most engagements use a combination — a direct accounting connection for the P&L, a CSV upload for management reporting, and a manual override for the handful of items that need explanation.

Path 1 — Xero Connection

For Xero customers, a single OAuth authorisation pulls the full general ledger, trial balance, and chart of accounts directly into the Valuator. The connection is read-only — the Valuator never writes back into Xero — and is scoped to financial data only, with no access to bank feeds, payroll, or sensitive employee data.

Once connected, the Valuator pulls the most recent five financial years of monthly data and lays them into the chart-of-accounts mapping layer. From that point on, refreshing the data is a single click — useful when the engagement spans a month-end or when a new set of management accounts becomes available mid-process.

What gets pulled: complete chart of accounts, monthly P&L by account, monthly balance sheet, trial balance, account categories. Tracking categories (where used) are imported as additional dimensions and can be used to drive revenue attribution.

What does not get pulled: transaction-level detail (unless explicitly requested), bank reconciliation data, employee-identifying payroll detail, customer or supplier-identifying detail beyond aggregated category totals.

Path 2 — QuickBooks Connection

The QuickBooks Online connection works the same way as Xero — a single OAuth authorisation, read-only scope, five years of monthly data, click-to-refresh. QuickBooks Classes (the QuickBooks analogue of Xero tracking categories) are imported as additional dimensions for revenue attribution.

For QuickBooks Desktop, the standard route is a CSV export from QuickBooks Desktop, uploaded via Path 3 below.

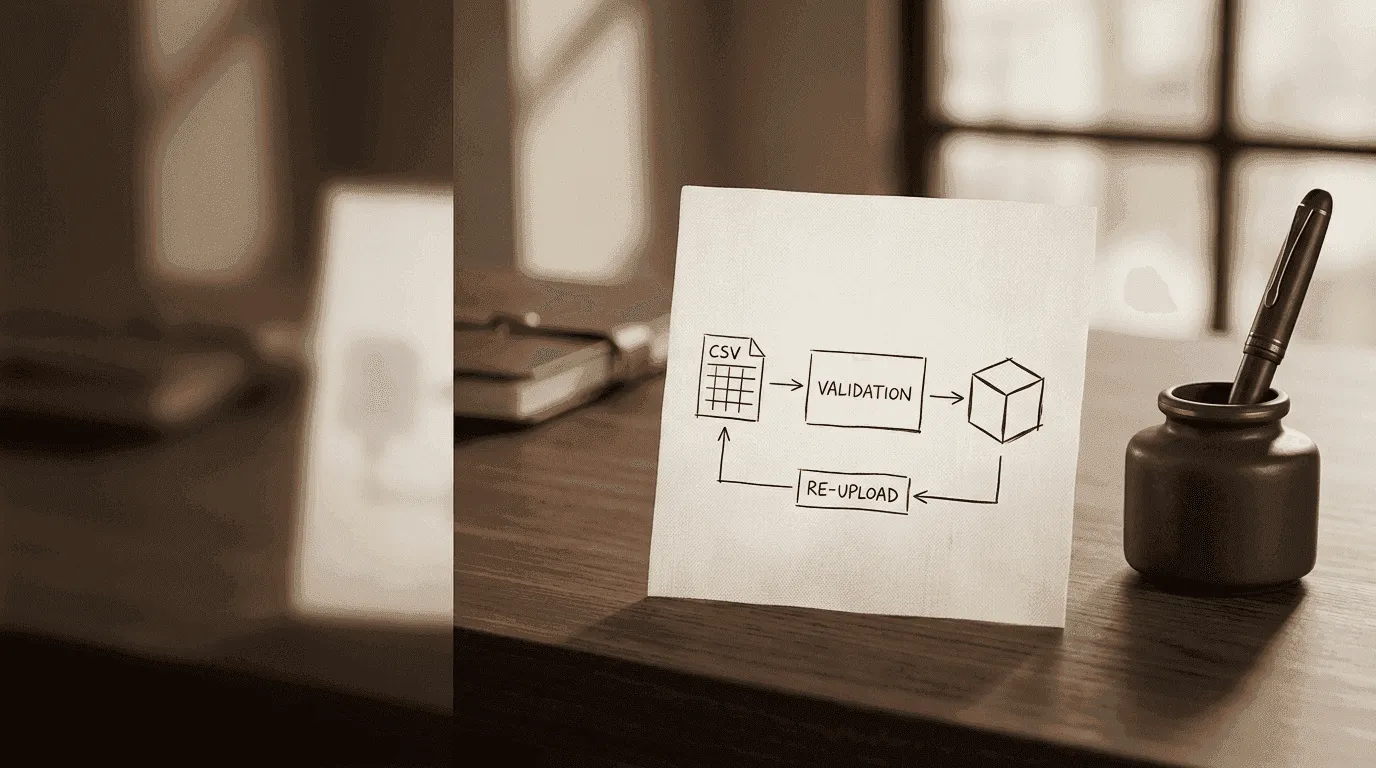

Path 3 — CSV Upload

For every other accounting platform — Sage 50 / Sage Intacct, NetSuite, FreeAgent, FreshBooks, Workday Adaptive, Excel-based management accounts — the Valuator accepts structured CSV uploads. Three CSV templates are provided in the import workflow:

- Chart of accounts — account code, account name, account category, parent account

- P&L by month — period date, account code, amount, currency

- Balance sheet by month — period date, account code, amount, currency

The templates accept the formats most platforms export by default. Where columns differ, the Valuator's CSV import wizard maps the source columns to the template columns at upload, and the mapping is saved for re-use on the next refresh. A typical first-time CSV import takes 10–15 minutes; subsequent imports take under a minute.

✔ Example

A UK SME on Sage 50 exports its trial balance and chart of accounts as CSV at month-end. The first time the data hits the Valuator, the CFO spends 12 minutes confirming column mappings and reviewing the chart-of-accounts categorisation. From the second month onwards, the same exports drop into the Valuator and the refresh completes in 45 seconds. The CFO uses the refresh to update a quarterly portfolio valuation that previously took a week of spreadsheet work.

The Chart-of-Accounts Mapping Layer

Pulling ledger data is the easy part. The harder problem — and the one that separates a useful import from an imported mess — is turning a chart of accounts designed for tax and statutory reporting into the inputs each valuation method actually needs.

The Valuator's chart-of-accounts mapping layer sits between the raw imported data and the valuation calculators. Its job is to map every account line to one or more of the following:

| Mapping Target |

What It Drives |

Typical Source Accounts |

| Revenue — total |

Top line for RFR, MPEEM, Greenfield |

All revenue accounts |

| Revenue — by segment / product |

Attribution for RFR, MPEEM |

Revenue accounts split by tracking category, class, or sub-account |

| Direct costs |

Gross margin, contribution margin |

Cost of sales, direct labour, direct materials |

| Operating costs — marketing |

Brand investment for Replacement Cost, RFR cross-check |

Advertising, marketing, sponsorship, PR |

| Operating costs — R&D / development |

Technology investment for Replacement Cost, Greenfield, capitalisation |

R&D, development, engineering, product |

| Operating costs — sales |

Customer acquisition cost for MPEEM contributory asset charge |

Sales salaries, sales commissions, sales tooling |

| Operating costs — administration |

Overhead allocation for With-and-Without, Greenfield |

Office, finance, HR, legal, IT |

| Workforce costs |

Replacement Cost (assembled workforce) |

Total payroll, on-costs, recruitment |

| Tax |

DCF tax rate |

Tax charge, deferred tax |

| Capitalised intangibles |

Capitalisation, audit trail |

Development costs capitalised, software cost capitalised |

For accounts that are unambiguously one thing — payroll, tax, statutory cost of sales — the mapping is automatic. The Valuator's mapping engine recognises the standard chart-of-accounts conventions used by Xero, QuickBooks, Sage, and the major UK and US chart templates, and pre-populates the mapping on import. The CFO or valuer then reviews the pre-populated mapping and adjusts any line that needs to be re-categorised — typically two or three lines per chart of accounts.

Once the mapping is set, it is reused on every refresh. The valuation does not need to be re-built when a new month closes. The same mapping turns the new month's ledger into the same valuation inputs.

ℹ Note

The mapping layer is the audit trail. Every input feeding every valuation method can be traced back through the mapping to the exact ledger accounts that produced it. This is the artefact a diligence team will ask for — and the one that is missing in most spreadsheet-based valuations.

Attribution: From Revenue to Asset-Level Inputs

The hardest mapping question in any intangible asset valuation is attribution. Total revenue is a single number on the P&L. The valuation needs to know how much of that revenue is attributable to the brand, how much to the customer book, how much to the technology platform, and how much to a non-compete or a contract.

The Valuator handles attribution through three mechanisms, applied in order of preference.

Mechanism 1 — Direct attribution from accounting tags. Where Xero tracking categories, QuickBooks Classes, or CSV-supplied segment codes already split revenue by segment, product, channel, or customer cohort, the Valuator uses those splits directly. This is the cleanest case — the attribution is already in the ledger, and the valuation just reads it.

Mechanism 2 — Allocation rules. Where direct tags are not available, the Valuator supports rule-based allocation. Revenue can be allocated across assets by published rules — for example, "70% of revenue attributable to the brand for licensed product lines, 30% to the customer book for direct-to-customer lines" — and the rules are saved with the mapping. The rules are explicit, reviewable, and travel with the valuation into the audit trail.

Mechanism 3 — Method-specific defaults. Where neither direct attribution nor explicit allocation rules are set, each valuation method falls back to a documented default — the FASB-conventional split for that asset type, calibrated to the business's sector. These defaults are flagged in the output, so a board pack or diligence response can name where attribution was derived from the ledger and where it was derived from sector convention.

The order matters. Direct attribution beats allocation rules beats sector defaults. A serious engagement uses Mechanism 1 wherever possible, Mechanism 2 for the gaps, and Mechanism 3 only where the underlying data simply does not support more granular attribution.

10-15

Minutes for first-time CSV import

<1

Minute per subsequent refresh

2-3

Mapping adjustments per chart of accounts

100%

Of inputs traceable to ledger

One Dataset, Every Method

The reason the import layer matters is that the same dataset feeds every valuation method the Valuator supports. The mapping is the single source of truth — change a mapping, and every downstream valuation recalculates from the same numbers.

Concretely, a single Xero connection or CSV upload produces:

Relief from Royalty inputs — revenue attributable to the brand or licensed asset, by year, for the projection period. The mapping converts the segment-tagged revenue into the brand-attributable revenue stream that RFR needs.

MPEEM inputs — revenue attributable to the primary income-producing asset (typically customer relationships), operating margin, contributory asset charges for workforce, brand, and technology. All four are computed from the mapped ledger. The contributory asset charges are not estimated — they are calculated from the same workforce, brand, and technology lines used in Replacement Cost.

Replacement Cost inputs — total cost to recreate each asset class. Workforce: total payroll plus recruitment plus ramp time. Brand: cumulative marketing spend over the relevant build period. Technology: cumulative R&D and development spend, with capitalisation adjustments. All three come straight from the mapped ledger.

With-and-Without inputs — the cash flow uplift attributable to the asset, calculated against a counterfactual scenario. The counterfactual is constructed from the mapped operating cost lines, with the asset's contribution removed.

Greenfield inputs — the full P&L for a hypothetical greenfield business owning only the asset in question. Constructed directly from the mapped cost base, with revenue scaled to the asset's attributable share.

Market inputs — comparable transaction multiples, applied to the mapped revenue or EBITDA line for the relevant asset class.

★ Key Takeaway

A defensible valuation across six methods that shares a single underlying dataset is fundamentally stronger than six valuations built off six different spreadsheet extracts. The mapping is what makes that single source of truth possible.

What This Means for the Engagement

Connecting the ledger to the Valuator changes the shape of an engagement in three ways that materially matter.

The first day stops being data wrangling. Engagements that previously started with a week of "send me a five-year P&L, send me the chart of accounts, send me the payroll summary, send me the marketing spend by year" instead start with a 30-minute Xero authorisation or a CSV upload. The valuer is reviewing mapping and challenging assumptions on Day 1, not waiting for accounts.

The output is reproducible. A valuation built off a mapped ledger can be re-run. New month closes; refresh the connection; re-run the valuation; track how the portfolio number has moved. This is the difference between a one-off valuation report and a managed intangible asset portfolio that compounds in usefulness over time.

The audit trail exists. Every diligence team that has ever questioned an intangible asset valuation has asked the same question: "Where did this number come from?" When the answer is "from the chart of accounts, here is the mapping," the conversation moves on. When the answer is "from a spreadsheet a previous valuer built," the conversation gets longer.

Worked Example: A B2B SaaS at Series B

A UK B2B SaaS company is preparing for a Series B and needs an intangible asset portfolio valuation for the data room. The CFO connects Xero to the Valuator on a Monday morning.

Hour 1. The Xero OAuth authorisation completes in two minutes. The Valuator pulls five years of monthly P&L, balance sheet, and chart of accounts. The mapping engine pre-populates 86 of 91 accounts; the CFO reviews and adjusts the remaining five (one re-categorised from "general office" to "R&D" to capture a dev-tools subscription line; two cost lines split between marketing and sales; one revenue line tagged as deferred rather than recognised).

Hour 2. The CFO sets revenue attribution using Xero tracking categories. The categories already split revenue by product line and by acquisition channel. The Valuator reads the splits directly — no allocation rules required.

Hour 3. The first valuation run completes. Customer relationships are valued under MPEEM, with the contributory asset charges for workforce, brand, and technology pulled from the same mapped ledger. The brand is valued under RFR, with brand-attributable revenue derived from the product-line tracking categories. Proprietary software is valued under Replacement Cost, with the technology investment line driving the buildup.

Hour 4. The portfolio rollup produces an aggregated intangible asset fair value, broken down by asset, by category, and by The Opagio 12 value driver. The methodology audit confirms the discount rate is consistent across all DCF-based valuations and that no contributory asset is double-counted.

What previously took a week of spreadsheet work has produced a defensible, reproducible portfolio valuation in half a day — with a complete audit trail that any Series B diligence team can interrogate.

How CSV and Xero Imports Connect to The Opagio Method

Data import is not a step of The Opagio Method — it sits underneath the method, as the data layer that every step depends on.

| Step |

What Happens |

What the Data Layer Provides |

| Discover |

Identify intangible assets across Opagio 12 |

The chart of accounts itself surfaces signals — capitalised intangibles, R&D spend, brand investment, customer concentration |

| Assess |

Score the maturity of each value driver |

Quantitative inputs (R&D intensity, marketing spend, customer retention) feed maturity scoring |

| Value |

Calculate the economic contribution of each asset |

Every valuation method draws on the mapped ledger as its single source of truth |

| Position |

Build the strategic narrative |

The audit trail from ledger to valuation underpins the diligence response |

| Optimise |

Monitor and grow the portfolio continuously |

Refreshable connections make ongoing portfolio measurement viable |

A method that requires its data to be re-extracted by hand every quarter is a method that does not get re-run. A method that refreshes from a connected ledger is a method that becomes part of the management rhythm.

Getting Started

The free Intangible Asset Valuator gives you an indicative single-asset read with no account required. Most users start there: pick one asset that matters to your business, enter the figures directly, and run the appropriate calculator. The data import layer is not required for that first read — it is the workflow that scales single-asset valuations into a portfolio.

For full data import — Xero or QuickBooks connections, CSV uploads, the chart-of-accounts mapping layer, and the audit trail that feeds every valuation method — Opagio Intangibles provides the complete workflow. It is the right tool for any engagement where the audience is external, the audit trail matters, and the valuation will need to be re-run as the business moves through funding rounds, exits, or annual reporting cycles.

If you have a transaction in scope and want to discuss whether a connected Xero or QuickBooks workflow is the right fit, contact the Opagio team for a complimentary scoping conversation.

Ivan Gowan is the CEO of Opagio. He previously spent 15 years at IG Group (LSE: IGG), where he was part of the senior leadership team during the company's growth from £300m to £2.7bn — a transformation driven overwhelmingly by intangible assets that traditional accounting did not capture. He holds an MSc in neural networks from the University of Edinburgh (2001).